Summary

This FAQ will be updated as questions arise. It is not a substitute for reading the policy itself, which contains full definitions, approval, and additional information.

SECTION 1: WHY THIS POLICY?

Q1: Why does WFAA need a quasi-endowment policy? What’s the benefit?

Quasi-endowments represent a significant portion of the Endowment Investment Portfolio. Because these funds are pooled and invested alongside permanently restricted endowments, decisions about one fund can affect all funds in the pool. The policy provides consistent, transparent governance to:

- Protect the stability of the shared investment pool and manage short-term liquidity risk – large or poorly timed withdrawals from quasi-endowments can force asset sales that hurt returns for every fund in the pool

- Ensure equitable treatment across all participating funds

- Apply UPMIFA’s prudent investor standards uniformly across all EIP funds – this reinforces WFAA’s legal and ethical obligations as a fiduciary

The goal is a sustainable, fair framework that protects all funds in the pool over the long term.

SECTION 2: THE LOCK-UP PERIOD

Q2: How is a quasi-endowment identified in the reporting I have access to?

The “Fund Class” in GFM (Gift and Fund Management) is Temporarily Restricted.

Q3: What exactly does the lock-up restrict?

The lock-up prevents withdrawals from the invested portion of a quasi-endowment for a period of five years from the date the fund was invested in the EIP. Any withdrawal requests made from the expendable cash portion of the fund are not subject to a lock-up.

Q4: When does the lock-up clock start—and does it reset when new gifts are added?

The lock-up begins on the date the fund is first invested in the EIP, which is always a quarter-end date—not the fund start date. A fund start date may be earlier for various reasons (e.g., the fund hadn’t yet reached the minimum, or a special handling code directed gifts to expendable cash). The clock does not reset when new gifts are added; it applies to the fund as a whole from the initial investment date.

Q5: What about funds established with 5-year pledges? How are those handled?

Assuming the pledge is for the endowment minimum, and the fund will not reach the endowment minimum until the last pledge payment is made, that fund’s lock-up period will start when the endowment minimum is reached, and the fund is invested. Pledge payments received prior to investment are held in cash to be endowed until fund minimum is reached.

This response only applies to newly created funds. If a fund was created on or after 7/1/2026 with a pledge commitment this response applies. However, if the fund was created prior to 7/1/2026 with a pledge commitment, then it will be exempt from the lock-up when the fund reaches endowment minimum and is invested, as the donor would not have agreed to a quasi-endowment creation with knowledge of the new policy.

Q6: Which funds are subject to the lock-up, and which are not?

The five-year lock-up definitively applies to quasi-endowment funds invested in the EIP after July 1, 2026. In other words, any endowed funds invested on September 30, 2026 are subject to the lock-up. Operationally, any funds already invested in the EIP on or before March 31, 2026 are definitively not subject to the lock-up. In most cases, funds invested in the quarter ended June 30, 2026 will also not be subject to the lock-up – however, See Section 4 for more information about how the transition window (April 1–June 30, 2026) will be handled.

Q7: How do I find out whether a specific fund is subject to the lock-up, and when it ends?

WFAA is adding dedicated fields in GFM (Gift and Fund Management) that will show: (1) whether the fund is currently in an active lock-up period, and (2) the lock-up end date. This is expected to be visible as of July 1, 2026.

Q8: Can exceptions to the lock-up be approved?

Exceptions must be approved by the Controller, in consultation with the Chief Financial Officer.

Q9: Does the lock-up apply to individual gift additions made to an existing quasi-endowment?

No. The lock-up applies to the fund as a whole, based on the date the fund was invested in the EIP. New gifts added to an already existing fund do not trigger a new five-year lock-up period for the entire fund.

SECTION 3: THE EXCESS WITHDRAWAL CAP

Q10: What is the invested balance of a Quasi-Endowment?

The invested balance is the total of the Endowment Book Value Account and the Cumulative Fund Value Adjustment Account, or Total Endowment Market Value.

Q11: What is an excess withdrawal?

An excess withdrawal is any amount requested beyond the fund’s expendable cash balance. For example, if the expendable cash balance is $25,000 and a disbursement of $85,000 is requested, the excess withdrawal is $60,000.

Q12: What are the two caps that apply to excess withdrawals?

There are two separate limits, and both must be satisfied:

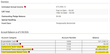

- Per-fund cap: A quarterly excess withdrawal may not exceed the lesser of (a) 80% of the fund’s current market value, or (b) the amount that would reduce the fund’s market value to the applicable minimum endowed fund level. Withdrawals that would reduce the fund below the minimum are only approved as part of a planned liquidation and closure. In the example below, the allowed excess withdrawal is the lesser of (1) the amount that reduces the Total Endowment Market Value to the endowment minimum in effect, which is $55,000 ($105,000 – $50,000 = $55,000) or (2) 80% of fund market value, which is $84,000. In this case the total disbursement is capped at $80,000 ($25,000 cash + $55,000 liquidated from invested balance).

| Expendable Cash | $25,000 |

| Disbursement Request | ($85,000) |

| Excess withdrawal | ($60,000) |

| Fund Market Value | $105,000 |

| 80% of Fund Market Value | $84,000 |

| Endowment Minimum | $50,000 |

- EIP aggregate cap: The total net excess withdrawals across all endowed funds in the EIP in any single quarter may not exceed 0.5% of the prior quarter’s total EIP market value. This applies portfolio-wide—not per fund—and includes all funds, even if invested prior to July 1, 2026.

| All funds: Excess withdrawals | $40,000,000 |

| All funds: Fund closures and liquidations | $5,000,000 |

| All funds: Cash to be Endowed received | ($40,000,000) |

| Net Excess withdrawals | $5,000,000 |

At the end of each quarter, WFAA looks at the total EIP market value from the prior quarter-end. The cap for the current quarter is 0.5% of that figure. For example, if the EIP was valued at $5 billion at the prior quarter-end, the aggregate cap for the current quarter would be $25 million in net excess withdrawals.

Net excess withdrawals is the total of excess withdrawals plus fund liquidations less any new endowed gifts received during that same quarter. If $45 million in excess withdrawals and liquidations were requested but $40 million in new endowed gifts came in, net excess withdrawals would be $5 million—which would be within a $25 million cap.

Q13: What happens if requests exceed the 0.5% cap in a given quarter?

If aggregate requests approach or exceed the threshold, the CFO and CIO have discretion over the amount and timing of disbursements which can be expected to be paid in subsequent quarters. This is anticipated to be a rare occurrence given the composition of our funds and historical precedence. Large request needs should be communicated to WFAA as early as possible to ensure the best planning and communication.

Q14: How is an excess withdrawal actually processed—what do the mechanics look like?

Excess withdrawals are processed through quarter-end liquidation. Here is how it works step by step:

- The request is submitted and reviewed by Finance.

- Finance confirms eligibility (lock-up status, per-fund cap, aggregate cap headroom).

- An initial disbursement is paid after the request is processed—this does not depend on waiting for quarter-end. It includes 100% of the fund’s expendable cash balance plus up to 80% of the fund’s endowment market value, as long as the 80% does not result in the fund’s market value dropping below the applicable fund minimum.

- A final disbursement of any remaining balance is paid by the 50th day after quarter-end, once the quarterly endowment close is complete and the fund’s final value is confirmed.

Q15: Can multiple smaller withdrawal requests within the same quarter avoid the aggregate cap?

No. The cap applies at the portfolio level across all funds. However, structuring requests over several quarters may make sense for large withdrawals.

SECTION 4: THE TRANSITION PERIOD (NOW THROUGH JUNE 30, 2026)

Q16: Does the new lock-up provision apply to funds that are already in process?

The answer depends on where the fund is in the establishment process at the time this policy is communicated.

For the purposes of this policy, a fund is considered “in process” if it has entered the fund establishment workflow prior to the policy communication date. This may include situations where a gift agreement has been drafted, is under review, has been sent for signature, or has already been signed and is awaiting final administrative processing, execution, funding, or investment.

- Funds already invested in the EIP on or before March 31, 2026 are not subject to the lock-up.

- Funds with MOAs signed by the donor prior to the communication of this policy are not subject to the lock-up period, even if final processing, execution, funding, or investment occurs after the policy communication date.

- Campus designated funds already in process when this policy is communicated and expected to be fully established and invested by June 30, 2026, will generally not be subject to the lock-up period, pending WFAA Finance approval.

- Funds already in process when this policy is communicated but not expected to be finalized by June 30, 2026 should be brought to WFAA Finance as soon as possible for exception review.

- Quasi-endowments initiated after this policy is communicated will be subject to the lock-up, even if they are documented or invested by June 30, 2026.

Q17: Can an excess withdrawal be requested before June 30, 2026 to avoid the new cap?

No. The aggregate net excess withdrawals will be monitored during this period, and the cap is intended to be honored even for the quarter ending June 30, 2026. If there is risk of exceeding the threshold, the CFO and CIO will be notified. Please provide as much advance notice to WFAA Finance as possible for any large disbursement needs.

SECTION 5: DONOR CONVERSATIONS

Q18: How should I explain the new lock-up to a donor who is considering a quasi-endowment?

The lock-up can be framed as a feature, not a restriction. The five-year lock-up is what allows the fund to be invested in the same high-performing portfolio as permanent endowments. A donor who commits to a quasi-endowment is making a long-term investment decision—the lock-up is consistent with that intent and protects the fund’s ability to grow. If a donor needs near-term access to the funds, a quasi-endowment may not be the right vehicle.

SECTION 6: ADDITIONAL QUESTIONS?

Q19: When should I bring WFAA into a conversation proactively?

Engage WFAA early by reaching out to your development liaison or submitting a ticket through the Help Center whenever:

- A donor or campus partner is discussing a new quasi-endowment—especially during the transition period

- A large or time-sensitive excess withdrawal or fund liquidation is being contemplated

- A callable fund conversion is being considered

- A fund agreement or gift instrument is ambiguous about whether principal is available to be spent

- Questions about whether an exception to any policy provision might be warranted

Q20: Will there be training?

There will be two information sessions offered in July.